Home sales drop 6% MoM, Housing Affordability Falls to More than 10-Year Low

Home sales drop 6% MoM, Housing Affordability Falls to More than 10-Year Low

Vito Scarnecchia- Broker, Realtor, DAD, Veteran

More Than a Third of US Small Businesses Couldn't Pay All Their rent!

homebuyers lose deposits of $10,000, $20,000, or more when canceling new home contracts

Housing Affordability Falls to More than 10-Year Low as Rising Interest Rates Take a Toll

5mm sold vs 6.2 mm Real Estate Sales Volume is down and will be in the future.

US home prices could crash 20% if the Fed fails to 'thread the needle' when tightening, central bank economist finds

The next 6-9 months will see the largest amount of home buyers enter the market

Oct existing home sales drop 6% MoM. That's the 9th straight month-on-month decline. Compared to last Oct, sales were down 28% YoY. They were down 38% YoY (!) in the West

What's your Favorite #REWTF? on Facebook? Check it out

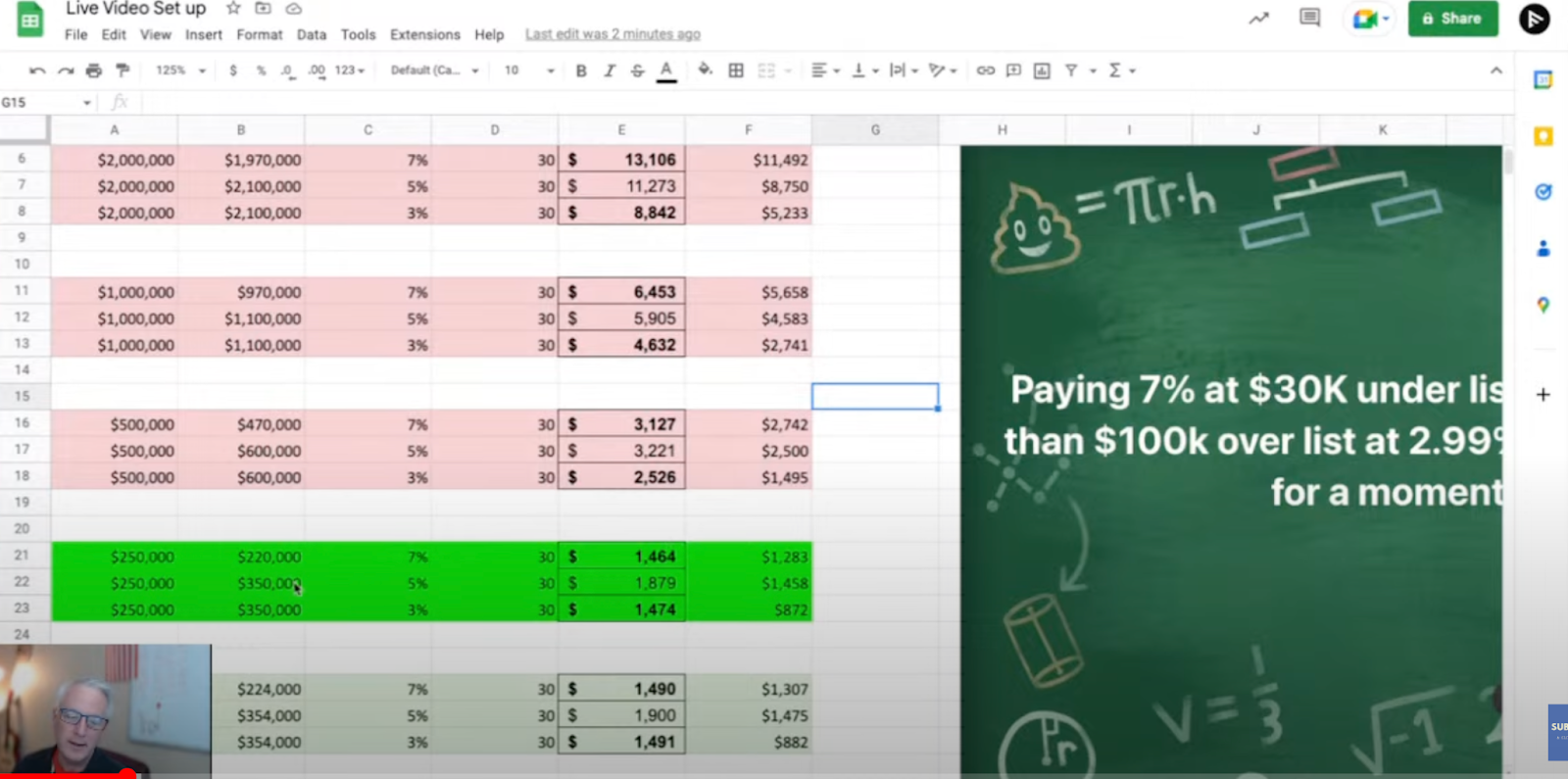

7% better than 2.99% sheet 8

More Than a Third of US Small Businesses Couldn't Pay All

Financial Intelligence

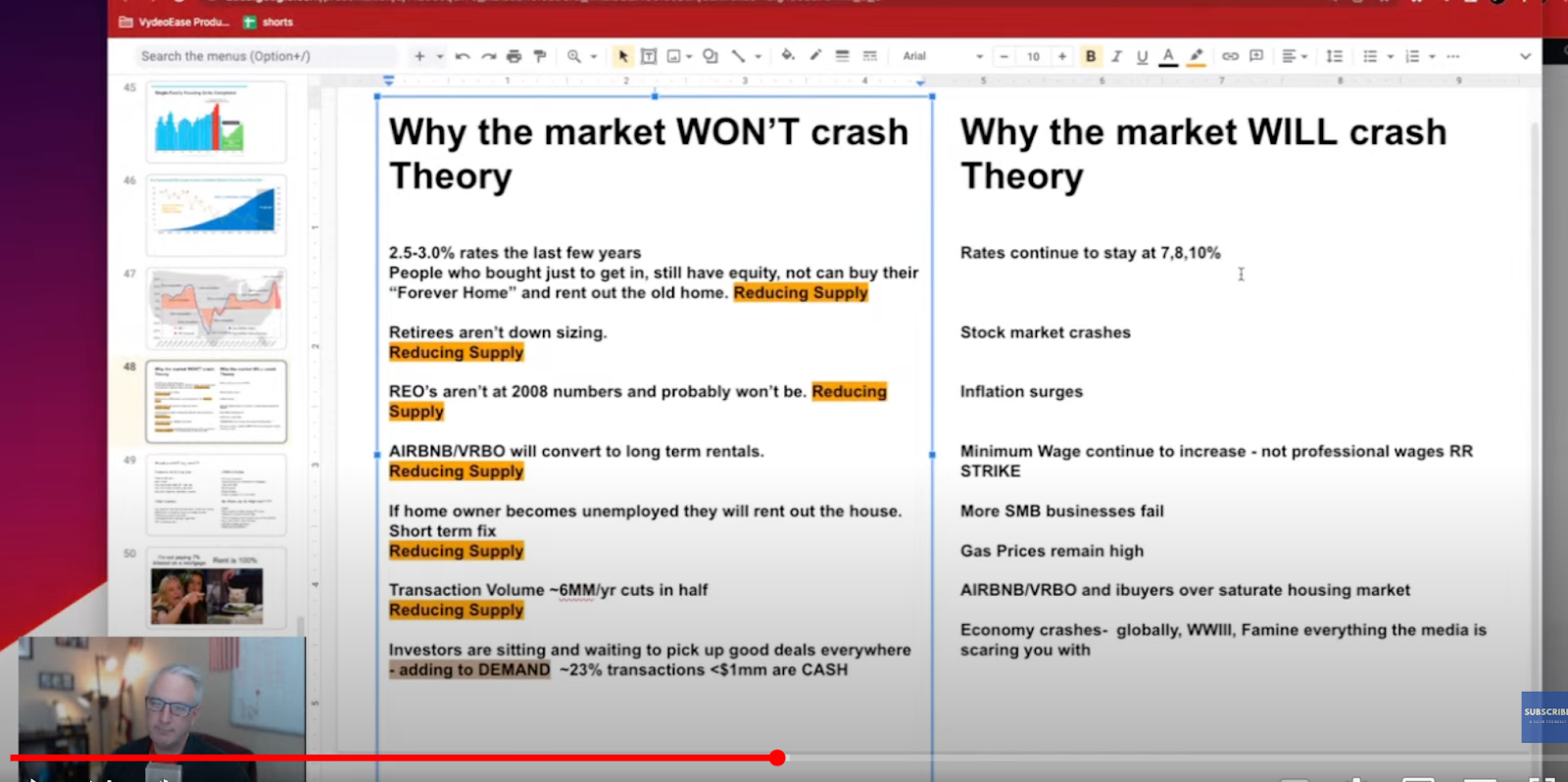

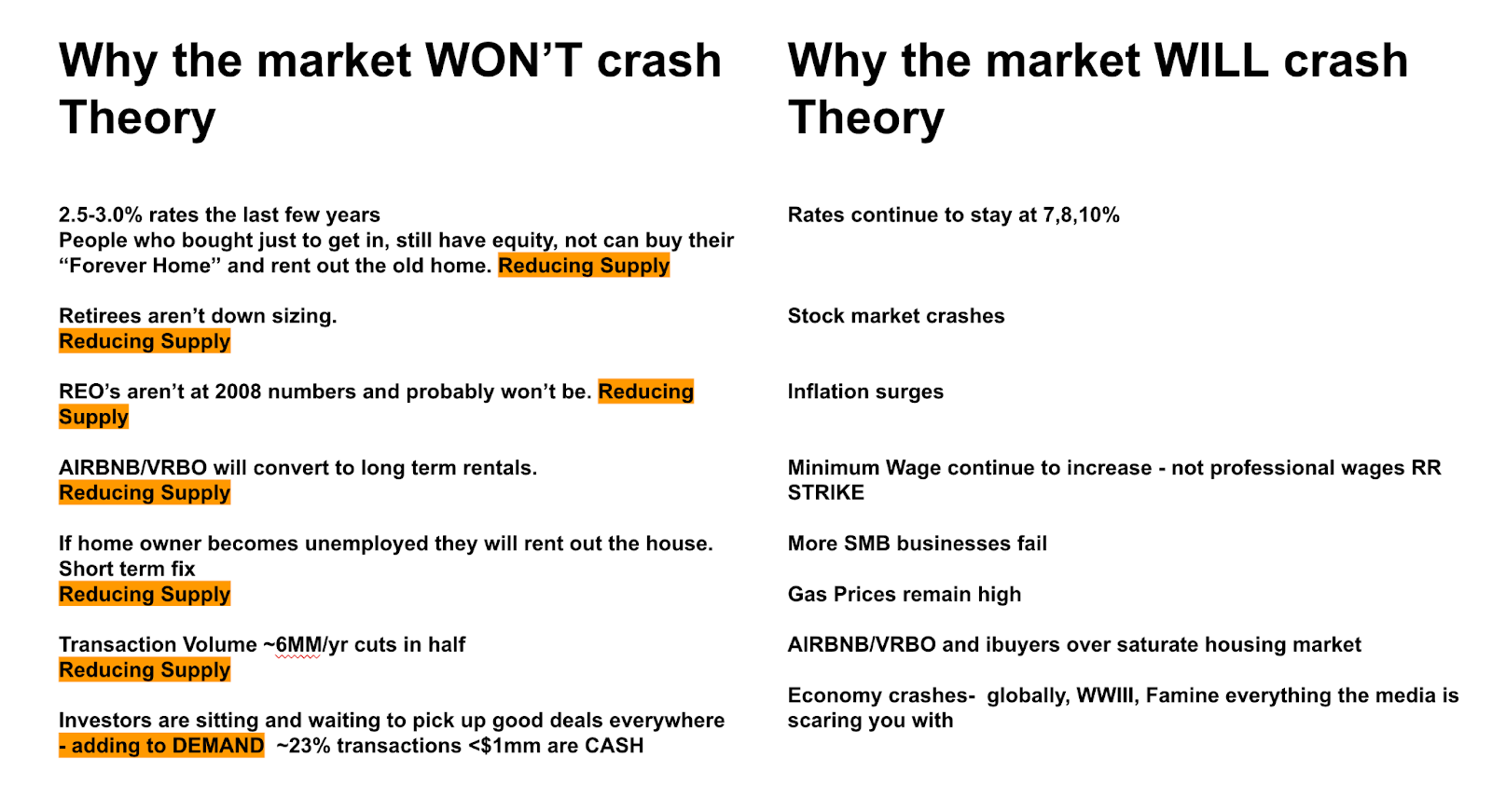

Plausible theory of why the market won't crash

car sales Volume

repo's are going up

Happy almost Thanksgiving. This market is so up and down right now, it's not even funny. And that's really what we're talking about today, where we're going, where the rates are going, where the market's going, everything talking about news, salacious news, headlines that have been taking root, especially when it comes to real estate.

We're also talking about some other things that kind of come into the whole “ Hakuna Matata” or the whole vicious cycle of this economy that we gleefully live in.

Is now a good time to buy?

I just posted this, I post a new video on this every Thursday. I think I did it last week, but this kind of goes through the whole mindset and process.

Is Now a Good Time to Buy a House?

If you're thinking about buying a house in the next year or two or three, now is probably the time and why? And yeah, we'll fill out some more information about that, right? So before we get into that, let me get rid of this because that's gone. We've gone through quite a few different weeks of this, haven't we?

Interest Rates

Rates are 6.6, actually looks like 6.654, but that's not a quoted rate, right? So it depends on who you go to. Talk to Hector or Scott or Louis. If you want to know what brokers will take what you have, your loan application and shop around for the best rates and best scenarios.

And they'll come up with a strategy. If you're all about rate, go to Bank of America. They always have great rates, but can't always talk about service. They want to. You want to close on time? There you go. If you want If you want great rates and like even Quicken loans is so far out of W right now, and these might be refinance late rates too, right?

There's a difference between home purchase and ra refi. And then also it depends on if it's a jumbo or not, which we actually have videos on. YOUTUBE.COM/@SiliconValleyLiving.

Gas prices are coming down a little bit.

Last week it was 4.63. Today it's 4.39. Of course, it's Costco and all over the place. The highest, though, is 5.91 in San Jose, and wouldn't you know it right? Santa Teresa High School is where the Shell Station has the highest price. It quoted at 5.91 is what I had it quoted at. So that was before. Looks like they rated it. Down. Yeah. See it was 5.91. That was three days ago, so now obviously it's down to 5.55. All right.

#rewtf

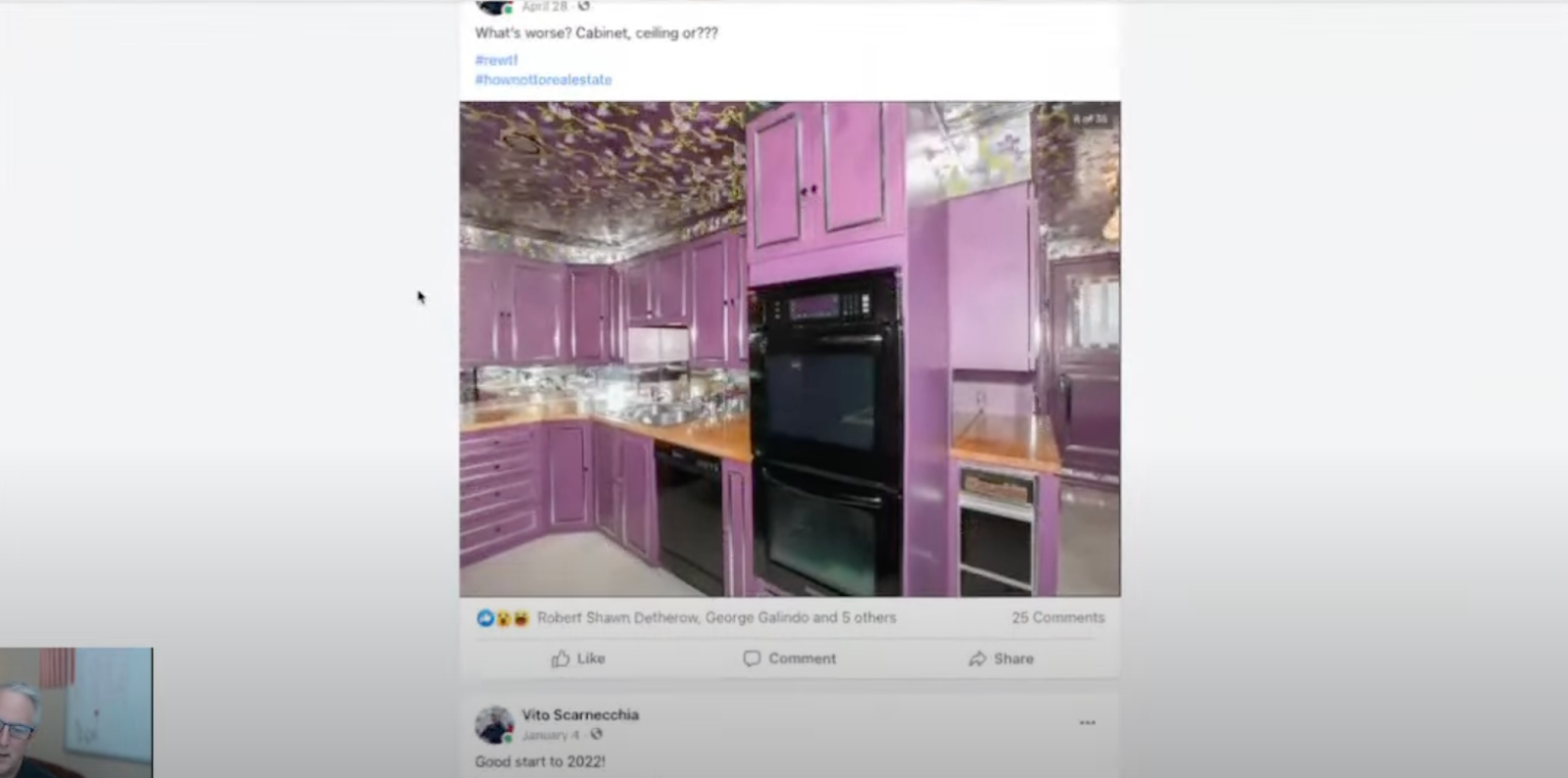

If you don't follow me on Facebook, I have this fun habit of posting pictures about different types of houses and what people do to them. And I want to have a look at that. That is just horrible. I wanna have a poll as to who can vote for the or which you what? Which of these pictures do you think is the worst?

Oh man. Just, it's amazing, and I'm looking at buying houses all across the United States and I see this stuff all the time. These are from posts . R E W T F. All you have to do is go to Facebook and type that in and look at all the fun stuff, and we're going to have a poll. If you're interested, let me know.

See past pics here: REWTFSalacious headlines, right?

Okay. So salacious headlines, right? People do stuff to get their attention. And when you read this, let me show you some of the posts that you see here. Lemme get there. See this right here. I have been seeing this post mostly probably because I'm in like real estate and I have connections with all sorts of real estate agents all across the United States.

7% is better than 2.99%?

Seems like a lot of 'em fell for this a little bit. Maybe they didn't fall for it, but they're like, oh, this sounds like a good idea. But they didn't really do the math. And, I think my math professors would say, Hey, Vito, you did a good job. You should have shown this formula.

Instead, I did it the manual way , because that's how I roll. This quote right here, 7% at $30,000 under list price is better than a hundred thousand dollars over list price at 2.99%. Let that sink in. That's a true statement up to a certain. So I did some math. It's definitely not 2 million, 1 million, 5 million, it's not even 5 million or 500,000.

See the meme's here CLICKIt crosses over about $254,000 Now, I don't know. You can't even buy I guess you could buy a mobile home, but that thing's going to be falling over for that here. It's hard to find houses for that price right now. So while. True for most places your 7% is going to be on par and these are fully amortized numbers, right?

Real Estate Brokers can’t pay rent?

So just take that with a grain of salt. Okay? Enough of that. You'll never see that again. I'm sure you also saw headlines saying real estate offices, one third of real estate offices can't afford to pay their rent. That's true, but if you dig into the root of where that headline came from, Bloomberg came up with it last week.

And it's actually businesses and I'm going to tell you right now a majority of those businesses are small and medium sized businesses. I'm sure there's a couple big ones. I'm positive that there's a bunch of big ones, but it was businesses, not real estate companies. I'm sure real estate companies are hurting just as bad as everybody else right now.

More Than a Third of US Small Businesses Couldn't Pay All

So I know people were out there saying real estate companies, because I think YouTube, not YouTube, Yahoo took it, this con, this headline, and converted it into real estate instead of just businesses. And ran with it, and then Acot went, and then all of a sudden real estate businesses are hurting.

Every business is hurting, but real estate businesses are in position, most of 'em, to weather out storms because oh, I don't know. Integrated circuit companies, semiconductor companies, electronic companies, they know for the last 40, 50 years that we go through cycles, up and down cycles.

Up and down cycles, right? And maybe there's a few companies out there that do comp electronic components that are hurting right now, but they're going to be around because they save up for a rainy day. Okay, so I agree with it, but it's just a headline, just like everything else. And the reason why I'm telling you this is because over the last week rates went down.

Interest Rates going to go down?

From 6.6 to seven, 7.1, 7.15 down to 6.65. I have a feeling the numbers are going to come back down to about five and a half, five, maybe on a good day, but it's going to float back and forth around March, December. January, maybe middle of February we'll start seeing it come down, but we're going to see rates stay this high for that long.

And then when March, April, or May comes around, then the buying season happens again, and then buyers are going to go back in the market regardless of the rate. But I can almost tell you with a fairly decent degree of certainty that you're going to see the price, the rates come. Considerably. Am I saying five, five and a half?

I'd like to see four and a half, but I think five is going to be the normal. Five is going to be the new normal. Five and a half maybe. So get that in your mindset. So don't hold out, because I'm sure we've talked about this a thousand bazillion times. Right now there's less competitive. If the market crashes, we're talking about that again today.

The market goes down a little bit. There's less competition right now. I hosted an open house this last weekend. I had 17 sets come through. Granted, a lot of 'em were neighbors by design. I wanted a lot of my neighbors to come by so I can remind them that I'm in real estate , right? Cause that's what I do.

But I had a lot of buyers. I wanna say eight or nine sets of buyers came through looking at them. Which is good. It's incredibly good. It's for Blossom Valley in my neighborhood. The last time I didn't open a house here, we had three show up, three sets show up altogether. So I think I can attribute that to one, the market picking up.

But also I cast a wide net of open house signs. I have 45, 40, plastic ones. And then I have a bunch of metal ones too. So I have over like a hundred, but typically I'm going to put out 20, 25, maybe 30. Open house signs for an open house. And the reason why is because one name recognition for me, right?

Housing forecast 2023

But also it attracts more buyers. I get more traffic than everybody else, so that's why. Okay. Yes. This one, Housing Forecast Update, Freddie Mac. Mortgage rates fall as inflation indicators ease.

Okay, whatever. It doesn't matter about inflation. It does, but it doesn't because, as we see the rates go up, you're going to see less houses being sold, but houses are going to come back down. And this, again, this is normal, we're not going to see two and a half, not until the next pandemic or the next whatever emergency thing that we're having to keep the economy moving.

The reason why we did that is to put made or offered up two and a half percent is because we needed to keep the economy floating. We needed to keep it moving. We needed to put money in people's pockets so they could go and buy stuff. So we kept the market going. The result of that was an unnatural increase.

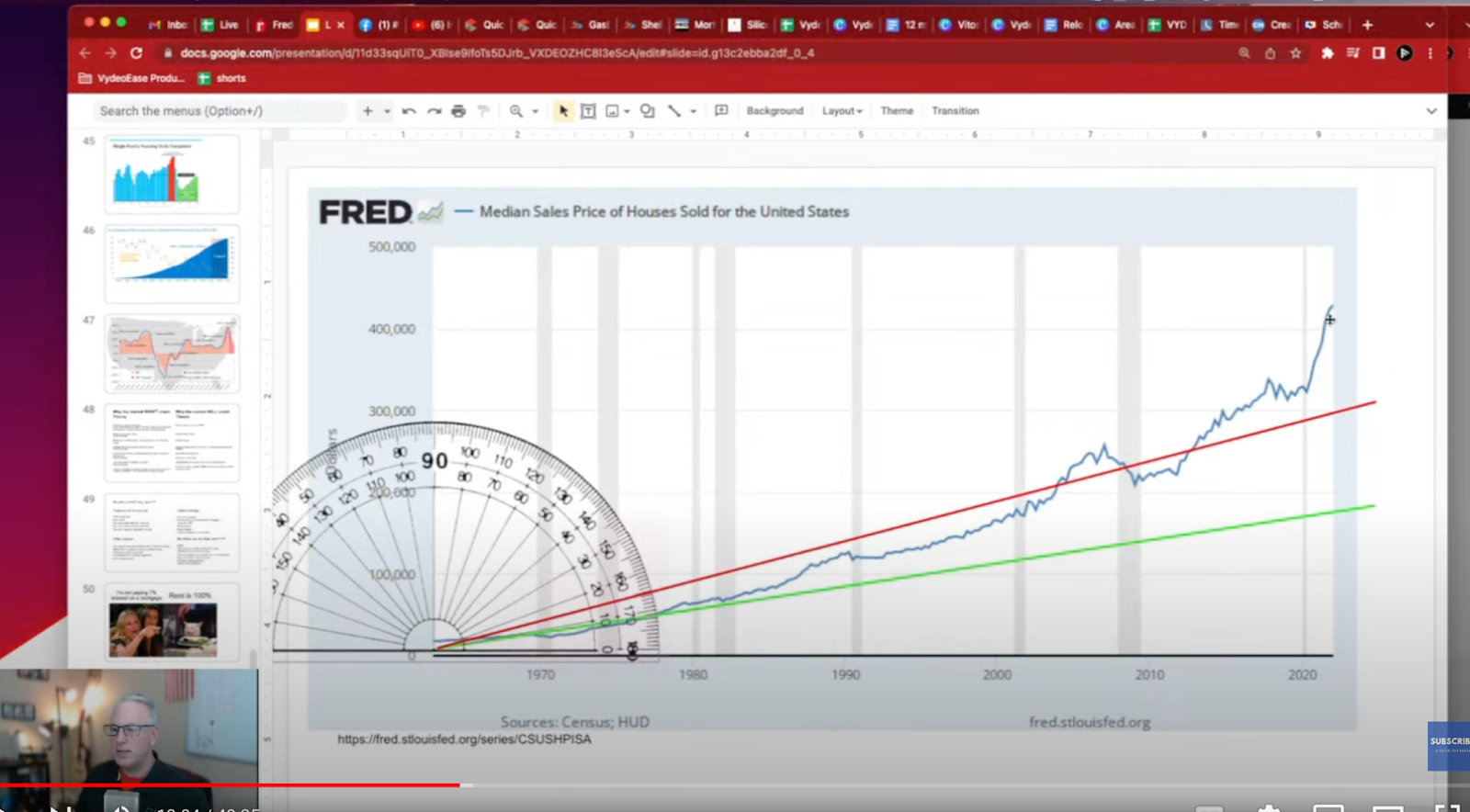

Right here. See, like this. If you look at this straight line, we'll go back to, where's my other one? There we go. This one's a little more accurate. That was 2008. Kinda came down a little bit. This one up the last two years have been an unnatural climb due to unnatural low rates. The low rates increased it, it made it more affordable and it didn't affect price.

It actually hurts pricing by increasing prices. So it pushed the affordability index down for every area in the United States. I can't say every, I wanna say most areas in the United States, most metropolitan and suburban areas, we saw massive up. So that's going to go down. Are we going to see a crash? I see it's going to flatten out.

Housing Values will come down

We're probably going to see this contract back down to its natural growth, which, I can't say that this is the natural path, but I'm just using that as an algorithm, as a analog. The end of the day you have to make that decision. I don't think we're going to do it. And here's another reason why.

My theory as to why, and this isn't mine, this is what a lot of other people are saying. And the same thing on this. This is what a lot of other people are saying, right? Why the market won't crash, why the market will crash, and their theories, right? They're just speculation. They're just people throwing out this is what happened in 2008.

Housing Market History

Oh, this is what happened in 1970 and this is what happened in 1980, and you know why I'm just throwing it out here so we can have a balanced argument or discuss. I don't know how many people refinanced or bought a house at two and a half, 3%. They're never going to be able to afford to sell it. It wouldn't make financial sense for them to sell it ever. Unless they need the cash. But then you can just pull out a HeLOCK, use that cash, put it back in, and then you're done.

Always keep that one. And if you notice right here, I'm going to keep highlighting this in orange. No. What did I want to do there? It is an orange. This is going to result in a reduction of supply of homes. Retirees aren't downsizing. They're choosing to die in their homes. Now why? Because the cost of moving is expensive.

Are some doing it? Yes. Are some choosing to? Yes. Are there other reasons why people are wanting to do that? Stay in their house or sell? Yes, absolutely. But on the majority we're going to see less retirees. People of my age move into a downsized home. This has been a topic of concern over the last five to 10 years.

Housing crash 2023?

We're just not seeing it.

Or even the multiple hundreds here, they're just, it's just not right. We're not going to see that. We're probably not going to see that, which again, reduces supply because there are no forced sellers. Airbnb, V R B O, I've been saying this for quite a while. They're going to either have to short sell it or sell quickly, Airbnb is failing them.

There's discussions about that. We're not going to go into that right now. They're either going to convert into long term long term rentals, or they're going to sell it off right now, and most of them bought into this one where it goes up here where they bought it, 2.5- 3%. They can't afford to get rid of it, so they're probably going to convert it into long term rentals if they're smart..

If the homeowner becomes unemployed, they'll rent out the house. It's a short term fix. If I rent, if I moved into my parents' house, I, if I got unemployed and I couldn't afford to make my payments, I would move out, move my family out, move my chickens out, move my dogs out, move them to my parents' house, in Knoxville, Tennessee, and rent this place out because I can rent it.

$5,-6,-7,000 a month and I'll pay off that plus a whole lot more reducing the supply, right? Smart people will do this. People that have their head in the sand and deny it until the very end. They're going to be the losers and we'll be out there to pick 'em up. Transaction volume, because of the rates right now, because of stock market crashes, because of this will merely slow down.

Right now, we're expecting that in the last 10 years, it's been about 6 million homes sold in America every year, which is a. We're expecting that to be cut in half. We're estimating that this next year we're going to end up with five and a quarter, 5.4 million homes sold. So we already see transaction volume or the supply dwindling.

All right. And then, Investors are sitting on the sidelines waiting for all this to come through and see if anything goes. They're looking for good deals. I can tell you that the many investors I know are looking for good deals right now. They're not buying on the I need to buy this house right now, or the time ticketed one, or just not doing that there.

They're sitting and waiting, being patient, and you wanna call 'em vultures? Sure. That's what they do, but they're also sobbing a problem. This adds to demand. I know my economics professor would tell me, you did a great job, but where's the math ? I'm a net sheet guy, , I'm a spreadsheet guy, not a math guy.

Lowering demand or lowering supply and demand stays steady or goes down just a little bit, or Wayne prices stays at the same. They don't go way down. Prices are pushed up.

That's why it won't crash. Our prices are going to go back to normal. Are we going to see a contraction? We are already seeing that we are already seeing a contract. I can tell you that my house was close to 2 million back in April, and now I'd be hard pressed to sell it for 1.7. As a matter of fact, the same house, two doors down, two blocks away.

Been on the market over 90 days at 1.7, probably 1.86 right now. Can't sell it. My house is in better condition, but that's not really relevant right now. So prices are contracts. It was a house. The house. I did the open house this weekend. 1.4. It's been on the market. 18, 19, 20 days now.

That wasn't happening. We're talking about. Hours, homes, being on market for a couple days on average, 12 days now we're seeing 31 days. So there's, it's not that homes aren't being sold, it's not that buyers aren't buying, it's just that smart buyers are buying right now because they've been waiting and they were frustrated when they had to deal with where it is?

Should you buy a house now?

17 buyers per home. When there's one buyer for 17 homes, they can be picky. If you're a buyer right now, you can be picky. If you wait till March, April, May, I can't promise that. I'm not saying that the market's going to turn around. We might go into a worldwide debacle, right? Go back up here. Here's why.

Rates continue to stay at seven, eight, even 10%. Some people are saying it might go up to 10%. The feds could go. 5% instead of 0.5 basis points, which is half a percent of stock market crashes. Stock market rallied this last week, but that's probably because of the elections, I'm not sure.

Inflation surges again outta control. That means we can't control it and this can't, this might be us, it might be North America, it might be. Northern hemisphere, or it could be global. There's a lot of reasons why inflation could surge. Here's a contentious one, and I'm sure that people will get pissed off at me saying this minimum wage continues to increase.

I'm not talking about professional RA wages or labor wages like contractor, construction workers. I'm talking about minimum wage. I'm talking about the demise of the franchise. Fast food chains. Newsom just increased the minimum wage, $22 an hour. That means you're going to be paying $20 for a sandwich.

You're going to be paying five to $6 for a drink because rent goes up. Utilities. Oh yeah. By the way, utilities are going up and wages are going up. Insurance is going up. The cost of living is going up for that business owner, and I don't care if it's McDonald's or Panera or the subway, it doesn't matter if it's $22 an hour.

Minimum wage and demise of fast food restaurants

And you have an average of 10 people per shift. You're looking at all two, 2.3 million at 15. Do $15 an hour. When it's $22, it's tw, I think you're like close to $3 million per year just on labor alone. So your profit just goes out of the way. And if I was a franchise owner and I owned a McDonald's, first of all, it would cost me two and a half million dollars to build a McDonald's of my own.

And I don't know if you know this or not, but that McDonald's over there, which I never patronized, I don't eat McDonald's, it's outta business. That jock in the box is outta business. There's another one that's out of Burger King on Saratoga. Sunnyvale. That's, I grew up there. I started working, I started that burger King back in the 1980s when I was a kid.

It was my second jobI helped open that store and it's gone. Now, I think they're turning it into a noodle house, which is fine. Whatever the noodle houses. Our mom and pop shops and they're, they don't have the same regulations. Plus they also make their kids work for $5 an hour.

It's just so they're going to survive. They're going to do fine. It's the franchises with over hundreds of employees, that kind of thing, where they're going to have that and that's going to hurt the economy overall. We're going to see major wage improvement everywhere because of. Everybody's yeah, that's great.

I can afford my million dollar house now. No, because when you can afford it and you make, let's say $300,000 now, and then it goes, you're every, you go up to $350,000 a year. Everybody else is going to go up to $350,000 a year. That means you can afford a little bit more. So then the upward pressure to buy a house goes up.

That means there's more buyers at that price range, and you're going to have to overbid for that. And there's more competition. So again, you're going to have 17 buyers for every house, so that can help continue to crash this market. More small and medium size businesses fail. We already talked about that in the headline.

But because of what's going on, we are going to have that. And that's a natural attrition right now. It happened in the sixties, it happened in the seventies, it happened in the eighties, it happened in the nineties. It happened. the.com smashed small businesses. the.com bust smashed small businesses. And it happened in the tens.

Now it's the twenties and we're going to see it again. It happens one out. I think half of every small business, new startup business fails within the first three years, two, three years. So normal thing, it's the same thing with real estate agents, right? You have about a 50 cent, 50% chance of making it out to your third year, and after that, then you're good.

You're gold. You're probably okay, right? That's this one right here. We're going to see this happen. It's a natural attrition, but you're going to see. Gas prices remain high. I don't think five and a half dollars a gallon is sustainable. And I know that there's a certain people, a set of people saying you should go electric.

I agree. And we're going to go into that in the next live show. We do. We're talking about it because we're running outta time now. We're talking about sales car volume, car sales volume, and car repo. And Tesla's up there and I go, oh, Tesla, whatever. I don't care if you're a Tesla fan or not. Electric cars are there, but they're not at the volume they need to be.

Airbnb, V R B O have oversaturated the housing market. That's already happening. If you hadn't heard open doors selling off. Assets. Redfin just closed their doors. They're starting to sell their assets. All the Iyer platforms are selling off. One company did it. Oh, no, it was Zillow. They had $400 million worth of homes.

In the Sunbelt corridor, right from Arizona to Florida. Sunbelt, $400 million worth of homes. They sold it to BlackRock or some kind of big holding company. Those houses will never see the market again. Those will always be rental markets, right? So these people are going to sell in excess and supply will go.

Global Crisis? WWIII? FAMINE?

Demand will consume them, but at a lower price. And the last thing that will crash our market is global economic crash or world war III or famine and pestilence and all the stuff that the media is scaring you about. Is it possible? Sure. But I don't think we're going to see it yet unless we have zombie apo.

We already have that with the Fentanyl stuff. I know that's not a thing to laugh about, this is a zombie apocalypse. If we get hit by an asteroid or what have you, that's something that possibly can happen. If World War Three breaks out, it can possibly happen. Everything goes on hold then.

All right. So enough of that. Let's see. I want to talk about this again. We're putting this thing together. It's going to be a webinar to give you a general Survey of what we're offering, right as we're bringing in a bunch of professional services to talk to you about understanding how to get your life into control.

Now more than ever, it's important for your household budget. Setting aside for the future, investing, buying real estate, that's what I do. If you have a business, talk to us. Insurance business, insurance person, healthcare stuff, dos and don'ts. If you're an employee, you can talk to his business insurance person to talk to him about what you, what things you should know going into a hospital.

Asking about costs of whatever issue you're going to go through. How do you work with those people? What kind of questions should you be answering? That's what this financial intelligence is about. We don't do this in school. We don't do this in high school. We don't do this in college. We surely don't do it in the military.

Very few families talk about it. So if you're interested in learning more about this, the whole concept is just pure education. There's no hard sale. We don't put you in a room and make you sign up or pay for anything. This is more we give you information and you do with it what you want. If you wanna work with us, yay.

Great. But what I've noticed is all of US professional services, financial advisors, realtors, lenders, business, whatever, we all work in these little silos and we all have separate information. What we're coming together is creating a plan for you so you can go from today to next year to five years to 10 years, and know where you're going to be without setbacks or what have you, and have a.

And be fully aware of what goes on in every step, and that's the whole idea of what financial intelligence is about. If you wanna learn more about it, let me know. Happy to bring that over to you. We're going to have a webinar and then we're going to invite you to an in-person Seminar Pro process where we do four or five classes at a time.

40 days on the market Report.

The whole reason why I started this, we're down from last week, so for the last few weeks we've been down. I don't know why I didn't do it that week, but whatever 90 days on market it's continuing to grow.

Again, this isn't because. The market's collapsing. I'll explain why this is down right now. Okay. People are buying houses, natural consumption. I think that level's coming up a little bit, but not to the, what we're expecting. But we're going to see buyers be a little more picky about what they're buying, how much they're paying for it, and sellers have to come to grips with that, right?

Res 24. It's not anywhere near the high, we're steadily going there. In 2008, we had hundreds of res, it took up like 10, 20, 30% of our inventory were res, are bank owned homes. After they foreclose on you, they take 'em back into their system. They own it. They sell it off to the secondary market and they have these loan, these guys that just sell houses at a fast clip.

That's all they do. But it's not happening because this is all of California, not all of California. That I can have my hands on. Is there certain parts of the desert that I can't get to, et cetera. The median home value in the US went down another $5,000. Is that scary? No. I've been telling you this for a while.

I'm going to get rid of this. The high was 416,000. But if you look at that chart, it's because we were so unnaturally high for so long. Now we're coming back down, right? We're correcting. If you look at today's numbers, what's that number? 380. 380. 380 is about right there. Okay. So yeah, we're contracting. We're contracting quite a bit.

That's all of us. If you look at just San Jose, we've contracted what, quite a bit too, by 200,000 really 34,000 on average. The last week over week, year over year, it's about a hundred and change, 150,000. So we had 70 closes last week. Compared to 135, we're seeing a 53% drop in transactions. When you see all these thumbnails saying the housing crashed.

Exactly what I did. Where did I put that?

Oh, this one. No. Home sales are down. That's what I want to talk about. Home sales are down. That's right. The volume of home sales are. The value of homes are going down a little bit, but not like a travesty. I don't think the Bay area's going to see a huge dip in 2008. We didn't see it at all. We did, but we went back to a natural number, right?

Median price 1.4. We're still above the less on average, which we're still above the less priced sales price ratio, we haven't seen anything dip below 98, 90 7%. It's not huge. I don't think these numbers are that bad, which you have to look into and I can show you these numbers real here. Real. All these numbers, this is list price to sales price, right?

Not the original price, but the current price to the sales price Of those, where is it?

25%, 24%. Were over a hundred. So we're still seeing homes sell for over list price. As a matter of fact, a hundred seventeen, one oh two, one oh six, one oh eight, one fourteen, the high was 117. The low was 75%. Let's take a look at what that house looked like. I don't think I can find it, but I will get the address for sure.

Maybe next week. I'll get you that, those numbers. I don't see the 75 here.

All right. Without boring you. I'll go, I'll find that number for you. Days on market are now at a month. That's still pretty good. Still a seller's market. Pendings 45 were down from the last few weeks. Sales li. Sales price decrease is 162, which is 44% of what's on market in San Jose. This price decrease is 160.

No, that's right here. 100, 1 62. Tft back on market is 38. So 38 cancellation contract cancellations. And then we had the actual listing. Cancellations. The listing canceled or expired or withdrew. We had 21 of those. So on average we get, we see about 34 a week over the last few months. And I'm not going to go through each and every one of these, but what I want you to look at is all these red numbers in this column C, those are home.

Those are the areas that have inventory contracting. Of all the few that I'm looking at, three of 'em are not contracting. Does that mean the market's back? I don't think so. I don't, I think the market's kind of limping along. I think the market's still going at 50%, right? 50% of what it was last year.

I think we're back to normal. And I think we're slower than normal. I think we're going to see it tick up. Once rates get back. Once rates get down to five, five and a half percent, you're going to see. Volume increases, obviously, but you're also going to see supply dwindle because if you look at these numbers, Cape Coral, back when I first started looking was 2283, right?

There's $1,200, 1200 more, over 1200 more, right? 620. Everything's going up over the long haul. 29 to 36. All the numbers are going up, but the week over week is going down a little bit, and I'll tell you why. Winter?

Yeah, winter. It's not the season. Our season to sell in a majority of the United States and metropolitan areas, they're selling season is March, April, may. It has been since I've been in real estate and since before that, since before I knew anything about real. Over the last two years since Covid started, there was absolutely no stop.

There was zero stop. I'd be in a listing appointment and they would ask me, when's the best time to sell? And I would say it usually is March, April, may. But for right now, it's crazy. It was a wildfire, it was a firestorm. And now we're picking out. Cause it's done. Nothing lasts forever.

And quite frankly, I'm glad because working with buyers they actually get a reprieve right now. So is it time to buy? Not going to tell you yes or no, but I'm going to tell you that. You should definitely consider about Consider it. All right, I'm going to continue to do this. I have a few more things that we're going to talk about and I'll do that in my next live because I think we're running outta time and patience and it's 40 minutes.

And I hope you have a happy Thanksgiving on Vito Scarnecchia with The Abitano Group, powered by Compass. We’ll see you out there.

17 houses for each buyer: https://youtu.be/Dlmmfj3shW0

https://anchor.fm/siliconvalleyliving

Vito Scarnecchia

Realtor®, Broker, Veteran, Dad

DRE#: 01407676

Website: abitano.com

UPDATE YOUR HOME VALUES HERE

If you are moving ANYWHERE in the world - Let me know! I know a LOT of AMAZING Agents!

Book appointments here: https://calendly.com/abitano/15min

Home Buyers Course

IG https://www.instagram.com/abitanogroup/

FB https://www.facebook.com/vito.scarnecchia/

LI https://www.linkedin.com/in/vito-scarnecchia/

POD https://spotifyanchor-web.app.link/e/oxdH1Hwfcvb

Professional Photography by Kim E https://photosbykime.com/

Compass site: https://www.compass.com/agents/vito-scarnecchia/

VydeoEase.com- Post production service for business marketers.

Video Marketing Course for Realtors

housing market today,housing market crash 2023,home prices 2023,interest rates mortgage today,home values are dropping,home sales collapse to 10 year low,does home sales close,best real estate agent near me,redfin,realtor,silicon valley homes,should I sell now,should i buy real estate now,should i sell real estate now,should i buy investment property in 2022,is it a good time to buy an investment property,median house price

Comments

Post a Comment